ONE sales pipeline grows to 180+ opportunities

Our health tech Investment Oneview (ASX: ONE), just released its Q3 quarterly report.

Cash receipts were slightly down relative to Q3-2024 (the previous corresponding period) mainly because of delays in the renewal fee for a US$2.01 million deal.

Total cash receipts were ~€2.7m (A$4.8m) for the quarter.

The revenue churn and volatility is somewhat expected as ONE transitions its business model from hardware sales to a more bring your own device (hardware) led sales model.

So the thing we always look out for with ONE is more around deployments with new customers (or growth in logos)...

On that front ONE added another new customer logo, Kennedy Krieger in the US - which operates a 70-bed inpatient facility serving children and adolescents nationwide.

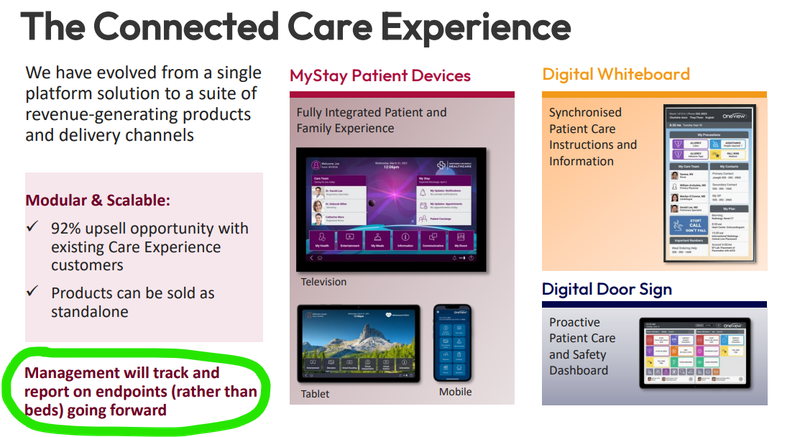

Across the quarter ONE added ~850 endpoints and is on track to exceed 15,000 total live “endpoints” by the end of 2025.

Endpoints is just another way of saying “beds” - which we think is a lot more applicable to ONE given the change in its business model.

I.e selling a digital whiteboard/digital doorsign and the BYO device solution isnt so much selling to a single bed, but more like selling to any room in a hospital so “Endpoint” makes a lot more sense.

(source)

ONE also said that it was in several discussions with potential new customer logos “before year-end” and reaffirmed that it was expecting to hit 15,000 live endpoints by the end of CY2025.

(we did see ONE mention it had 180 different pipeline opportunities so it will be interesting to see what comes from those)

(Source)

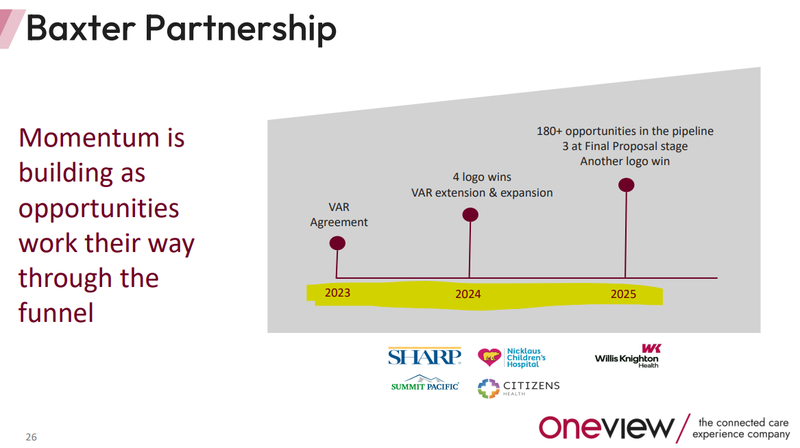

Hopefully, some of that pipeline is coming off the back of ONE’s partnership with $17BN New York listed Baxter International.

Baxter is one of the biggest suppliers of products into hospitals including hospital beds so we have high hopes for what comes from the partnership between them and ONE.

The deal between ONE and Baxter has been live since ~2023…

Baxter is one of the biggest suppliers of products into hospitals including hospital beds especially in the USA - so if ONE can start converting that sales pipeline into “endpoints” it could be very material for ONE.

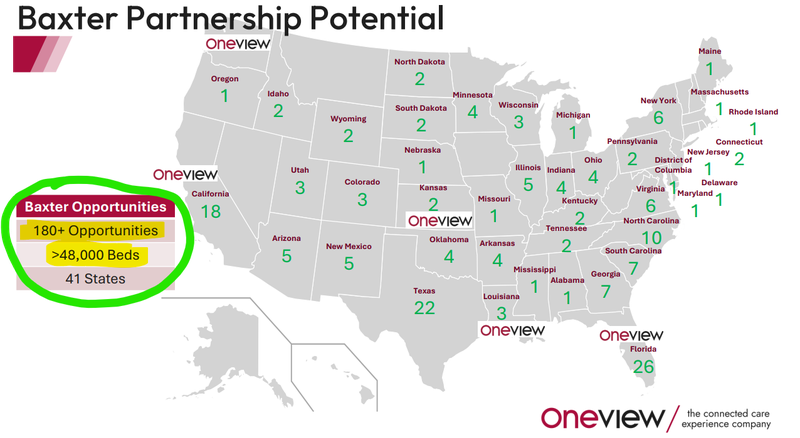

The following slide from ONE’s most recent presentation shows just how big that opportunity is - 180+ opportunities, >48,000 beds:

We also saw on LinkedIn ONE’s CEO James Fitter was presenting at a Baxter led conference with Baxter’s president for connected care.

The key takeaway for us from that is that Baxter still see’s ONE as having a place in whatever offering they are providing to their customer base…

What’s next for ONE?

🔄More contracted beds and logos:

More contracted beds and a transition to the more smoothed out revenue streams of a true SaaS model with MyStay.

ONE is reporting these in terms of “Endpoints” now, so we will be looking out for that number going forward.

Hopefully some of those late stage discussions can convert into big new logo additions for ONE over the coming months.

🔄Launch of pilots for ONE’s AI virtual assistant tech:

After today’s news ONE can bring forward the market launch of it AI virtual assistant tech.

We want to see the product officially launched and being trialled by customers.